Qualifying to

Labuan Corporate Tax Framework

References:

1

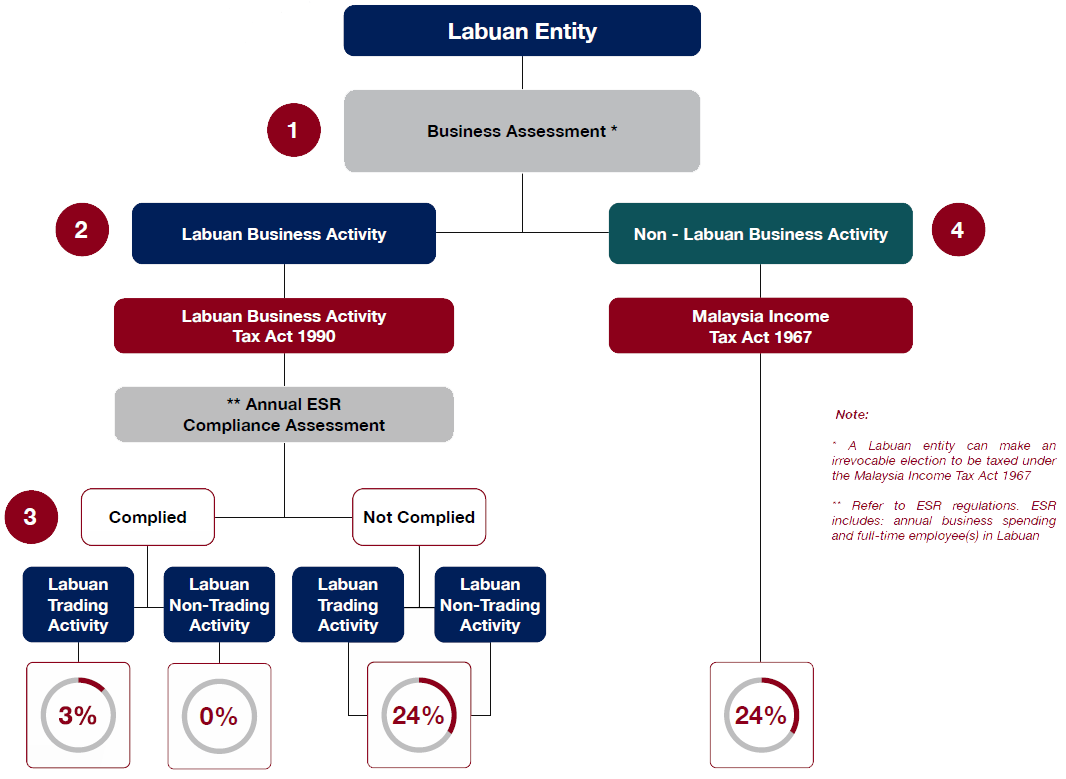

Undertake business assessment to determine if the intended business is a qualified Labuan business activity as prescribed under the relevant Economic Substance Requirements (ESR) regulations.

Non-Labuan business activity refers to activities not prescribed under the relevant ESR regulations.

Non-Labuan business activity refers to activities not prescribed under the relevant ESR regulations.

2

Determine the ESR for the intended business to qualify for Labuan tax framework.

3

Undertake ESR-compliant assessment to determine the annual tax treatment.

For a Labuan entity that does not comply with the ESR, the tax treatment for the respective year will be at the rate of 24% upon its chargeable profit. Chargeable profit shall be the net profit as reflected in the audited account.

For a Labuan entity that does not comply with the ESR, the tax treatment for the respective year will be at the rate of 24% upon its chargeable profit. Chargeable profit shall be the net profit as reflected in the audited account.

4

For a Labuan entity that undertakes non-Labuan business activity, the entity will be taxed under the Malaysia Income Tax Act 1967.